Talking About the Stock Market (5) - How Should a Retail Investor Think About Gold?

Preface: I wrote this "Talking About the Stock Market" series from the perspective of an ordinary retail investor and non-finance professional, as a small memorial to more than ten years in markets. Data shows what happened in the past, but it can still serve as reference for decisions today. The thinking behind indicators is worth revisiting.

Over the past decades, the highest annual gold gain was about 31%. But in 2025, gold was up more than 60% (as of Dec 9), breaking history. While the broader index struggled around 4000, gold approached 4400. The ChinaAMC Gold ETF (518850) was up 50%+ this year (as of Dec 9), likely beating most retail investors. Looking back at my daily stress selecting stocks and timing entries, reading reports, chasing rumors, waking up at night to check U.S. markets—honestly, it may have been better to just go all-in on this ETF at the start of the year.

First, even for professionals, gold is hard to model. Xiao Lin discussed this too: short-term drivers like speculation and risk-off are hard to quantify. Where is a "reasonable" price? When is it overbought? Institutions struggle too. So the best you can do is watch a few basic indicators.

So, as an ordinary retail investor, what can you track?

1. Gold Price

- USD-priced gold futures: search for COMEX Gold (GC00Y) in Eastmoney; trades nearly 24/7.

- RMB spot price: search AU9999 in Eastmoney.

- USD Index: add it to watchlist too; the basic logic is that a stronger USD tends to pressure USD-priced gold (USD up → gold down; USD down → gold up).

- Historical gold prices: data from the World Gold Council is authoritative and free.

2. How to Check "Central Bank Buying Gold"?

- Visit: SAFE

- Navigate: "Statistics" → "Foreign Exchange Reserves" → "Official Reserve Assets"

Link: SAFE - Official reserve assets - Choose HTML format

You can compute month-over-month changes yourself. For example, in Nov 2025 the central bank bought another 30,000 ounces. As long as the central bank keeps buying, the market tends to believe the long-term story is okay. After a pause for a few months last year, it resumed buying small amounts monthly—almost like a DCA behavior. When gold was around 2000, the buying was more aggressive; now it is more like "a symbolic purchase".

Note: central bank buying is strategic reserve management (hedging USD credit risk), not like retail trading. Historically, the central bank has not sold gold. Lower buying recently could mean USD risk looks manageable in the short term, and gold price is high. But these stats are lagging; who knows what they will do later.

Also: the chart shows official FX reserves (excluding gold) around $3.3T. The last similar high was in 2014 (~$4T), and within a year A-shares saw a big bull market. The simplistic logic: massive reserves stabilize the RMB exchange rate, which is foundational to attracting foreign investment. Many people are bullish on China's 2026 stock market; this may be one underlying factor.

3. Gold-Silver Ratio

Basic logic: gold and silver are often co-produced. Using 2024 data, for every 1 jin of gold mined, about 10 jin of silver is also mined. So the "factory ratio" is 1:10. But gold is globally treated as a quasi-currency and core asset, so the market ratio historically ranges around 1:50 to 1:80:

Historically:

- ratio < 50: silver may be relatively expensive vs gold; gold looks better value

- ratio > 80: silver may be relatively cheap vs gold, or gold may be overbought; silver-related exposure may be more attractive

- ratio 50–80: both can be considered

Over the past 20 years, when the ratio breaks above 80:1, silver's average gain over the next 12 months was ~35%, with peaks over 100%. Often, in the later stage of a gold bull run, silver catches up quickly. Some argue that silver is basically a leveraged trade on gold's main uptrend.

4. Debt and Macro Backdrop

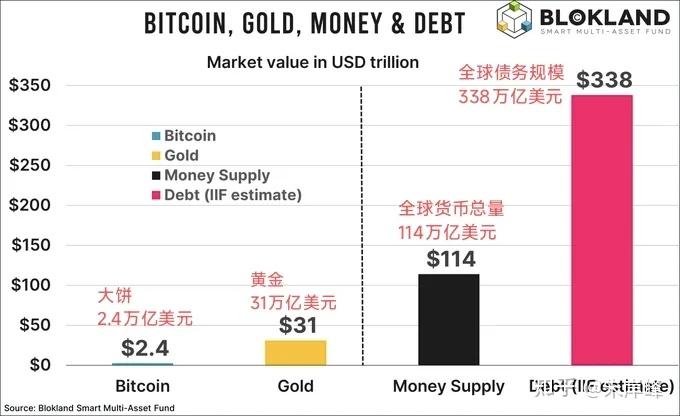

One common view: the surge in gold and silver reflects a global bet on a major credit downturn. Global money supply is around $114T, while global debt is about $338T—~2.94× global GDP.

Many countries run persistent deficits. The U.S. is a typical case, where even interest costs feel heavy. The 40-year debt-driven growth model may be approaching its limit.

Some argue gold correlates with U.S. debt-to-GDP (roughly inversely with credit). With higher uncertainty in U.S. GDP (trade wars, AI bubbles, etc.) and already high debt, risk-off sentiment pushes gold higher. The old saying "buy gold in chaotic times" still seems to carry weight.

5. Closing

On Oct 7, 2025, Goldman raised its Dec 2026 gold target from $4,300/oz to $4,900/oz. But the -5% big down day on Oct 22 may take time to digest: some statistics suggest after a -5% day, the probability of fully recovering within 60 days is below 30%. As of Dec 10, price indeed has not retested the Oct 22 high.

To push gold further, we likely need even stronger risk-off sentiment.